Chapter 3.2: Everything Important About Corporate Climate Targets

Published July 24, 2020

In June 2019, the UK government set a net zero emissions target for 2050. It was the first government to set a net zero target, and it is currently grappling with how to reach it. Businesses must adapt to the UK’s new 30-year ambition. The business community was an important voice that lobbied the UK government to legislate the target. However, a September 2019 survey by YouGov found that one-third of businesses had no plans to reach net zero emissions.

Failure to incorporate the net zero target into long-term business planning exposes organisations to regulatory and reputational risk. Investors and customers are increasingly using sustainability in their selection criteria for choosing who to do business with.

Setting a corporate climate target is an important first step in the development of a decarbonisation strategy. The exercise in setting a target helps embed within an organisation important processes for measuring and managing climate impacts.

Science-based and net zero targets are two popular choices of corporate climate targets. This guide seeks to define each and explain how they are set, their advantages and disadvantages, and which may be best for businesses to adopt.

If a business is considering a climate target, the target will invariably be a quantifiable emissions reduction target. It is important to use a robust emissions accounting protocol and have a grasp of the data used to gauge climate impacts in order to quantify GHG emissions and the results of efforts to reduce those emissions.

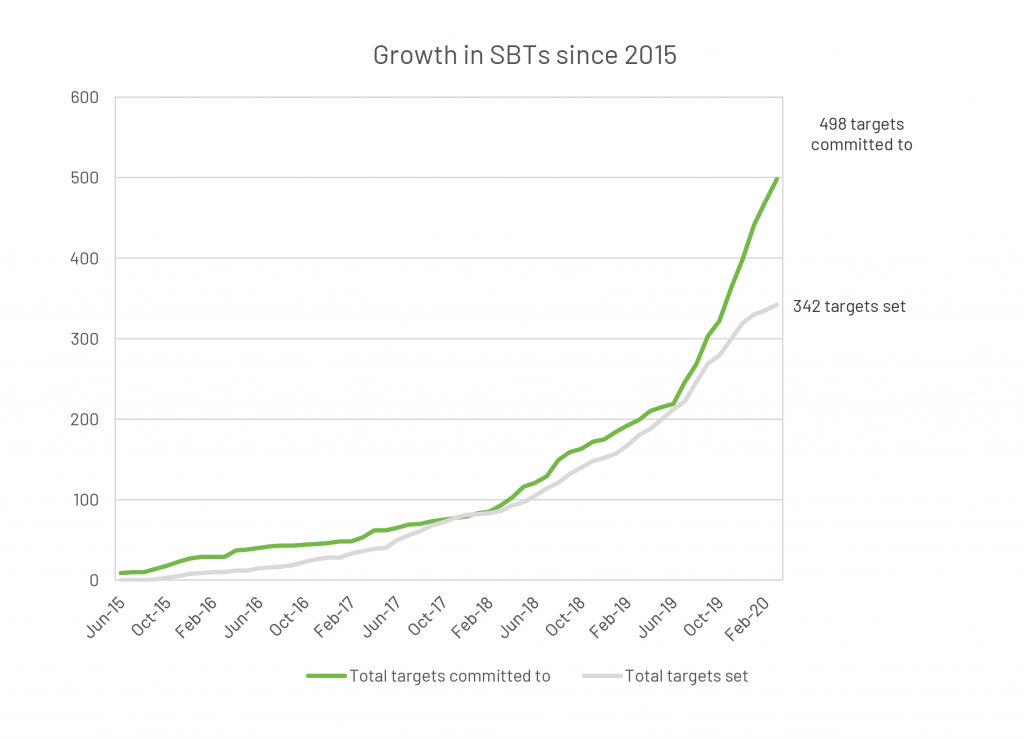

Science-based targets

Science-based targets (SBTs) are ones which align with climate science. They are rooted in the Paris Agreement. This is the (nearly) global consensus on which climate policy is based today: that global heating should be limited to 2°C (and ideally 1.5°C) to avoid the worst effects of climate change. SBTs represent corporate action aligned with the global consensus on what is necessary to develop sustainably.

SBTs are accepted and validated by the Science-Based Targets initiative (SBTi). The organisation checks targets against company data and criteria and assigns a level of ambition to the target, corresponding to:

- 1.5°C compatible

- Well below 2°C compatible

Until late 2019, the SBTi assigned a third category of ambition to SBTs: 2°C compatible. Research by the Intergovernmental Panel on Climate Change (IPCC) in 2018 detailed the anticipated impacts of 1.5°C and 2°C of global warming. The difference of 0.5°C is profound, and implies millions more climate refugees, ice-free arctic summers occurring ten times more frequently, and a doubling of the proportion of the global population exposed to extreme heatwaves at least once every five years. These insights led to the SBTi withdrawing its criteria for the 2°C level of ambition in its targets.

Obtaining an SBT involves five stages:

- Committing

- Developing

- Submitting

- Announcing

- Upgrading

The development stage can last no longer than two years. If the target is approved, it is announced by the SBTi, and the organisation with the target is promoted and enjoys reputational benefits. Some organisations have already met their targets or have set 2°C targets. These organisations can work with the SBTi to upgrade their targets.

There are two main methods through which SBTs can be set: the sectoral decarbonisation approach (SDA) and the absolute-based approach. A third, called the economic-based approach, is being developed. Each uses different guidelines to judge whether a target is compatible with a 2°C world.

The SDA uses the International Energy Agency (IEA) 2°C scenario (2DS), which characterises decarbonisation pathways for different sectors to aid in setting targets. It is useful for non-diversified businesses occupying a homogeneous sector.

An example of a validated SDA SBT is the one set by Ørsted. The group committed to reduce its Scope 1 (direct) and 2 (upstream electricity) emissions 98% per kWh by 2025 from a 2006 base year. It also committed to reduce Scope 3 (indirect) GHG emissions 50% by 2032 from a 2018 base year.

The SDA can only be used to set well below 2°C targets.

The absolute-based approach outlines minimum percentages in absolute emissions reductions. It uses guidelines from the IPCC Fifth Assessment Report RCP2.6 subcategory to suggest a decarbonisation pathway and requires a 49% to 72% absolute emissions reduction by 2050 from 2010 levels. An absolute-based approach might be chosen by a diversified company that does not find a niche for itself within the 2DS scenario modelling used by the IEA.

An example of a validated absolute-based SBT is Mars’s target to reduce its value chain emissions 27% by 2025 and 67% by 2050 from 2015 levels.

Another approach, called the economic-based approach, links global GDP with a carbon budget for 1.5°C or 2°C of warming. Corporations are given a share of this carbon budget based on the equivalent shares their gross profits have of global GDP. Targets can be set using this method once more detailed guidance is released by the SBTi.

Net zero targets

Net zero should first be defined. The Office of National Statistics defines net zero in the context of the UK’s 2050 economy-wide target as follows:

‘Net zero means that the UK’s total greenhouse gas (GHG) emissions would be equal to or less than the emissions the UK removed from the environment.’

A definition of net zero in a corporate context is not precise enough if ‘the UK’ is substituted for ‘a company’. Key missing elements are the scopes and boundaries of the emissions being considered in the zero-sum calculation.

Once the scopes and boundaries are defined, a net zero target can simply be a date by which any absolute emissions are countered with equal carbon offsets. Roughly half of global GDP is currently produced in areas where a net zero target has been legislated, is in a policy proposal, or is being discussed by a government. This is a much larger proportion than that covered by SBTs. In contrast to SBTs, net zero targets accept a ‘net’ result, rather than an ‘absolute’ one. In other words, carbon offsetting through purchases of carbon credits can be used to satisfy a net zero target. Carbon offsetting is controversial because it can imply no structural change for the emitter. Carbon offsetting is not permitted by the SBTi in meeting an SBT.

There is no governing body that judges net zero targets the way the SBTi exists to approve SBTs. One issue this creates is that organisations are free to define boundaries for their net zero targets that exclude significant emissions out of scope of the target. Scope 3 emissions are of particular concern. The Carbon Disclosure Project (CDP) in December 2019 released its Global Supply Chain Report, which revealed that supply chain emissions are on average 5.5 times greater than a company’s direct operations. The SBTi mandates that a carbon footprint covering the three GHG Scopes be considered when developing an SBT. If Scope 3 emissions account for at least 40% of Scope 1, 2, and 3 emissions, an SBT must include Scope 3 emissions reductions.

The appeal of net zero targets is in their apparent simplicity and their permitted use of offsetting. They are simple to communicate, in contrast with SBTs. They can be compatible with a 2°C or 1.5°C world when broad enough in scope and accompanied by an ambitious decarbonisation pathway. Organisations like the Net Zero By 2050 Team (a leadership group of CEOs and their companies) and the We Mean Business coalition exist to promote rigorous net zero targets.

Which to pick?

This guide has presented multiple options for corporate climate targets broadly classed into SBTs and net zero targets. Given the technical nature of SDA or absolute-based approach SBTs, obtaining validation from the SBTi is an attractive, although costly, way to promote the target. Alternatively, an ambitious net zero target can be chosen. While net zero targets enjoy popularity and simplicity, how they are reached determines their effectiveness. Ambitious decarbonisation pathways derived from climate science and that include absolute emissions reductions should be promoted as integral to net zero targets to ensure their effectiveness.

Ultimately, though, the two target types are not mutually exclusive (save for the prohibition of offsets in meeting an SBT) and can complement one another. The process of developing an SBT inherently involves rigorous methodology and can kick-start the process of embedding the processes in an organisation necessary to measure and manage climate impacts. This can also happen when setting a rigorous net zero target. Meeting an SBT implies structural change in the company that produces absolute emissions reductions. However, an SBT does not necessarily imply a net zero future. Accompanying an SBT with a long-term net zero target can be part of a robust decarbonisation strategy that allows companies to take a hierarchical view of emissions reductions along the following lines:

Tags Corporate Climate Targets IPCC Net Zero Targets Paris Agreement Science Based Target science-based targets